Retirement should be a time of relaxation and enjoyment after years of hard work. Yet concerns about the efficacy of the German pension system can cloud this golden period. The statutory pension in Germany aims to provide financial security to retirees. But understanding its details and your options is crucial, especially if you are worried about old age poverty.

You must be 67 to retire in Germany if born after 1964.

However, if you were born before 1964, you could retire earlier:

| Year of Birth | Retirement Age (years and months) |

| from 1964 | 67 years old |

| 1963 | 66 years and 10 months |

| 1962 | 66 years and 8 months |

| 1961 | 66 years and 6 months |

| 1960 | 66 years and 4 months |

| 1959 | 66 years and 2 months |

| 1958 | 66 years and 0 months |

| 1957 | 65 years and 11 months |

| 1956 | 65 years and 10 months |

| 1955 | 65 years and 9 months |

The retirement age is increasing because Germany’s population is aging. Hence, more people receive pensions for longer.

Increasing the retirement age allows people to contribute to pensions for longer. Plus, it also ensures that they receive pensions later on.

These changes reduced the financial burden on the statutory pension system. Some say we may see an even greater increase in retirement age in the future.

You could retire early, starting when you turn 63. That would mean you’d receive a reduced statutory pension.

You can expect your pension to decrease by ≈0.3% for each month of early retirement. This is a rough estimate from our calculations. Use the official state pension calculator to see how much your future pension will be.

Early retirement is appealing for those who wish to enjoy their golden years before the rest of the herd.

Still, prepare your retirement funds well in advance. You should account for smaller social security checks and extended retirement years.

It operates on a principle of solidarity. Contributions from workers fund the statutory pensions of retirees.

Employees and employers contribute a percentage of the former’s salary to the pension fund. Government subsidies also supplement this amount.

In 2024, the contribution rate is 18.6% of gross wages. Employees and employers each contribute 9.3% of the employee’s gross salary.

When it’s your turn to retire, you get monthly payments based on your contribution history.

There are 3 reasons why retirement planning is more critical than ever:

The sustainability of this pension provision system is under pressure. Germany’s population is aging, and its birth rates are decreasing.

If the imbalance between contributors and beneficiaries grows, younger generations will have to supplement their pension provision with alternative sources of income—for example, personal savings or investment plans.

Also, pension funds rely on their investments’ returns for cash. If they remain too low for too long, they’ll be forced to pause payments or ask the government for a bailout.

But what if this scenario doesn’t play out? Still, retirees need financial security if life events reduce their lifetime contributions. Yes, even things you can’t control could reduce your benefits.

Here are some examples:

But what if you’re confident in the sustainability of the system? And you know for a fact that you’ll maximize your statutory pension?

Well, you could have to downgrade your lifestyle.

Your pension will be smaller than your current salary unless you supplement it with additional retirement planning.

By now, you should be convinced that you must plan your retirement.

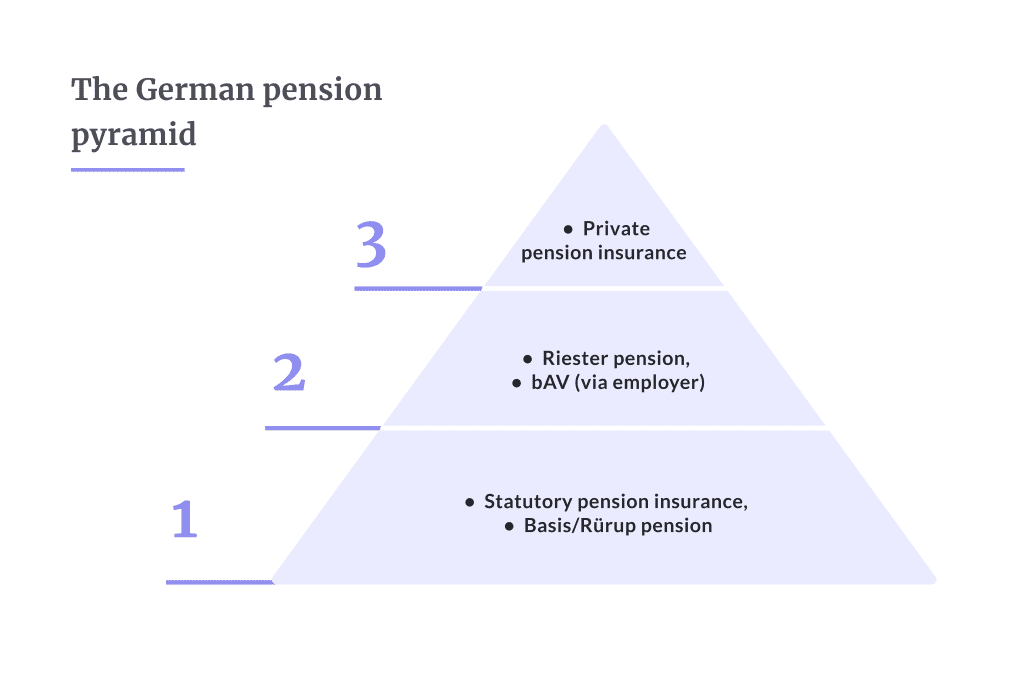

The German pension system is often compared to a pyramid. There are three levels, and as you go up the pyramid, you increase your financial security. The first level is the basic state pension, which provides a basic level of income in retirement. The second level is occupational pensions, which are provided by employers. The third level is private pensions, individual savings and investment plans.

So, what options are best for you? Let’s find out.

The Basic Pension, also known as the “Rürup Rentenversicherung,” after its creator, Bert Rürup, is a pension scheme introduced in Germany in 2005.

The Basis pension is designed to provide long-term financial and social security.

It’s best for the self-employed, freelancers, and high-income earners who aim to stay in Germany their entire career.

The Basis pension is excellent for self-employed and high-income earners in Germany long term. Its tax advantages and focus on lifetime income make it perfect for increasing retirement income.

However, private pension insurance is the better alternative if you seek flexibility or pursue a career outside of Germany.

The Riester Pension adds to the social security money you get from the state pension by encouraging you to save on your own, thanks to help from the state.

Former labor minister Walter Riester introduced it in 2002, but it’s lost its luster and has found many critics.

You contribute 4% of your annual gross income and get a yearly bonus from the government of 175€. If you have children, the government will add 300€ for each child you have.

If you contribute less than 4%, you’ll get some of the government’s contribution but not the full amount.

You also receive limited tax benefits from the money you pay into it. When people retire, they receive a regular payment for life from their Riester plan.

In 2024, the Riester pension has many disadvantages, making it attractive only for low-income earners with at least 2-3 children.

Company pension insurance (bAV) is when employees and employers team up to help save for retirement. There are five main types of company pensions in Germany:

Direct insurance is the most common option, so let’s explore it in more detail.

There are two forms of direct insurance:

In almost all cases, German occupational pensions are good for employees and employers.

They provide extra money for retirement and encourage loyalty from employees.

As retirement planning becomes more important, occupational pensions are a big part of Germany’s commitment to its workers.

Whether you’re an employee looking for job security or an employer wanting to offer good benefits, understanding and investing in company pensions is a decision for a better future.

Private pension insurance is a voluntary savings plan designed to build up assets for retirement. These plans offer tax benefits and flexibility in payouts.

Here’s what you need to know:

Private pension insurance is a versatile option. It’s perfect for enhancing retirement savings beyond mandatory pension schemes.

The private pension is like a personal savings account for retirement. You contribute money to it regularly, and over time, it grows. When you retire, you receive payments from this account. It could cover your living expenses, go on holiday, or anything you’d like.

You don’t have to live in Germany to take part in your pension insurance. You only need a European bank account, and receive tax benefits worldwide.

We recommend everyone consider private pension insurance. Well, anyone who wants flexibility and a decent standard of living in retirement is the right fit.

Planning for retirement in Germany involves understanding and utilizing various pension options.

While the statutory pension system is essential, supplementing it with private pensions, company schemes, or ETF saving plans enhances your financial security.

With its tax benefits and flexibility, the German private pension is a valuable tool for building additional retirement income.

Whether you’re at the beginning of your career or approaching retirement, integrating these options into your strategy will help ensure a stable and comfortable retirement.

ETFs (Exchange-Traded Funds) are a modern approach to retirement planning. They track the performance of specific indices and offer diversification and potentially higher returns than savings accounts.

ETFs are commonly used in pension plans, but you can invest in them independently.

An ETF saving plan involves making regular contributions to a portfolio of ETFs through a brokerage account. These contributions are invested in a mix of stocks and bonds, potentially growing over time to provide income in retirement.

How do contributions to pension insurance products work?In almost all pension products, you can choose the monthly contribution entirely. The more you contribute, the more money gets invested and the higher the payout.

How much should you contribute to pension products?We recommend contributing a total of around 10% of your income after taxes to all retirement saving plans you undertake.

What happens to my pension products if I leave Germany?This depends on the pension product you have because they work very differently.

It’s possible to get your pension back. For other pension products, it depends on what you subscribe to because they work very differently.